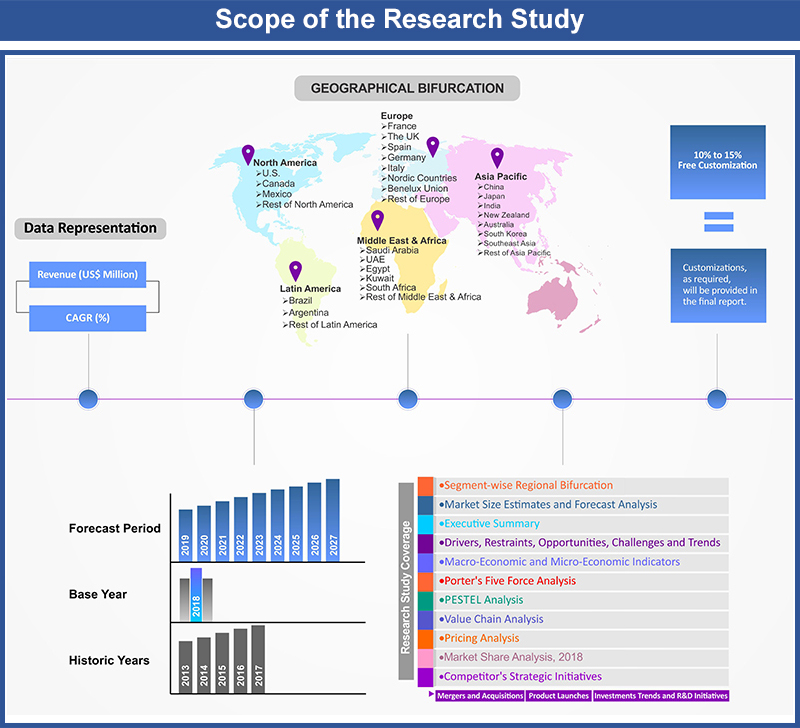

Mg-Al-Zn Coated Steel Market, by Type (Thin Carbon Steel, Conventional Carbon Steel, Thick Carbon Steel, Special Made Carbon Steel), by Application (Automotive, Construction, Industrial Heating, Ventilation and Air Conditioning (HVAC), Electric Power Communication, Specialized Greenhouse Structures, Others) by Country (The UK, Germany, France, Spain, Italy, Denmark, Finland, Iceland, Sweden, Norway, Belgium, The Netherlands, Luxembourg, Rest of Europe) — Europe Insights, Growth, Size, Comparative Analysis, Trends and Forecast, 2019–2027

Market Overview/Industry Trends

The magnesium aluminum and zinc (Mg-Al-Zn) coated steel alloys are the common type of heat treatable alloys used in various industrial sectors, including automotive, building and construction, electronics and telecommunication, amongst others. The coating of steel with magnesium aluminum and zinc as the formed alloy provides high resistance as the coating acts as a strong barrier and galvanic protection steel are used in the above stated industries. The growing demand among end-users for coated materials having high corrosion protection along with distinctive characteristics such as formability, joinability, and paintability is the most prominent driver for the growth of Europe Mg-Al-Zn coated steel market.

The composition of Mg-Al-Zn are available in different ratios, which included 93% Mg, 6 Al, 1% Zn (magnesium AZ61A), 96% Mg, 3% Al, 1% Zn (magnesium AZ31B), high zinc (93.5% Zn, 3.5 Al, 3% Mg), high aluminum (0.7%-3.4% Mg, 0.8-8.2% Zn, balance Al). Moreover, several functional qualities of Mg-Al-Zn steel also has a positive impact on the growth of the Mg-Al-Zn coated steel market. For instance, Zn-Al-Mg coating has a self-healing capability that imparts high performance and proper protection. The Zn-Al-Mg coating alloys possess improved microhardness, which provides better scratch and wear resistance. Furthermore, Al and Mg are light weight metals which results in less density of Zn-Al-Mg coating in comparison to the traditional coating of Zn. The varying concentration of Al and Mg in the Zn results in the formation of different Zn-Al-Mg coating which has different corrosion resistance properties. The increase in the concentration of Al in the Zn-Al-Mg alloy results in the formation of more corrosive resistive Zn-Al-Mg alloy. On the other hand, the composition with a higher proportion of Mg, as compared to Al, provides better corrosion resistance, however only to a certain extent. The Zn-Al-Mg alloy sheets are available in a different form, such as rods, foils, and other shapes, which results in wide applications across various industrial sectors. Thus, it aids towards the growth of the Mg Europe Al-Zn coated steel market.

The advantage of Mg-Al-Zn coated steel has also advantage over galvanized steel is that it protects the deformed shapes from corrosion, has a lower weight, and is formed through a simple fabrication process. Additionally, cost effectiveness of Mg-Al-Zn coated steel in comparison to stainless steel and aluminum is also having a positive impact on the growth of the Europe Mg-Al-Zn coated steel market. Moreover, it does not require post painting and reduces maintenance is also a driving factor for the market growth. Hence, the growing adoption of Mg-Al-Zn coated steel among manufacturers owing to its low cost and high corrosion resistance characteristics is contributing towards the growth of Europe Mg-Al-Zn coated steel market.

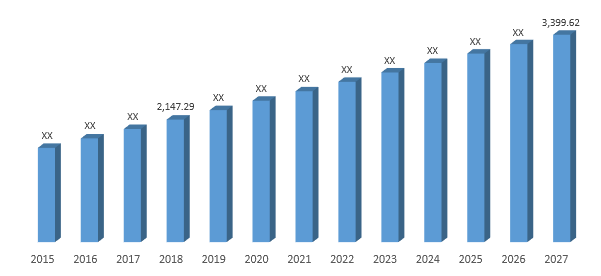

In terms of revenue, the Europe Mg-Al-Zn coated steel market was estimated to be US$ 2,147.29 Mn in 2018 and is expected to reach US$ 3,399.62 Mn by 2027 growing at a CAGR of 5.27% over the forecast period. The study analyzes the market in terms of revenue across all the major regions, which has been further bifurcated into countries.

Europe Mg-Al-Zn Coated Steel Market Revenue & Forecast, (US$ Million), 2015–2027

Type Outlook:

Thick carbon steel is expected to hold the largest market share and is anticipated to register highest CAGR during the forecast period. The volume consumption of thick carbon steel in the Europe Mg-Al-Zn coated steel market amounted to 92.87 Kilotons, which was also the highest in 2018. The high application of this steel in different mechanical, cutting and bearing applications is anticipated to be foremost factor contributing towards the growth of the segment during the forecast period, thereby aiding towards the market growth. However, special made carbon steel are expected to witness substantial growth rate during the forecast period.

The manufacturers are keen on increasing the adoption of the materials which are of low cost and are high corrosion resistant as it imparts better surface finishing and also has long lasting effects. For instance, ArcelorMittal S.A. has recently produced an exceptional metallic coating, Magnelis which provides better corrosion protection and it constitutes 93.5% of the steel, 3.5% aluminum, and 3.0% magnesium and is applied in hot dip process. Magnelis has corrosion resistance that it ten times higher than hot-dip galvanized steel, which makes it suitable for harsh environments and where long-term protection is needed. Additionally, the cost effectiveness of Magnelis is proving to be an alternative to stainless steel and aluminum. Thus, the growing dependency on the material which is cost effective and has high corrosion resistance is expected to drive the growth of Mg-Al-Zn coated steel market.

Application Outlook:

The construction segment is expected to hold the highest market share in the Europe Mg-Al-Zn coated steel market as Mg-Al-Zn contributed towards lightweight construction coupled with high durability. The countries in the European region are setting different standards which is the common technical rules for designing building and other civil engineering works. Thus, strong the building code in several European countries is also a factor contributing towards the growth of segment. However, automotive is the most lucrative segment and is expected to register highest CAGR during the forecast period. The increasing need of the manufacturers for low cost Mg-Al-Zn coated steel materials for the interior and exterior parts in the automotive industry is expected to be major factor aiding towards the growth of this segment, which is leading towards the growth Europe Mg-Al-Zn coated steel market.

Regional Outlook:

The countries in the Europe region are framing stringent regulations that are leading towards the high adoption of corrosion resistant sheets. The presence of key market players in the region, such as ArcelorMittal S.A, ThyssenKrupp AG, SSAB AB, amongst others in the region is also a factor that is aiding towards the growth of the market in the region. Additionally, the presence of key automobile manufacturers in Germany is leading towards the increased adoption of better corrosion resistant materials which has a positive impact on the growth of the Europe Mg-Al-Zn market.

The U.K. is expected to hold the largest market share during the forecast period. The presence of developed construction and automotive industry in the country coupled with the presence of strong building codes is a major driving factor for the growth of the Europe Mg-Al-Zn market in The U.K. However, Belgium is expected to showcase highest growth rate during the forecast period, followed by Denmark. The string government regulation regarding the construction of building in Belgium is contributing towards the growth of the segment, which is aiding towards the growth of the Europe Mg-Al-Zn market.

Competitive Landscape

The report provides both qualitative and quantitative research of Mg-Al-Zn coated steel market as well as provides comprehensive insights and development methods adopted by the prominent market players. Some of the key market participants in the Mg-Al-Zn coated steel market are ArcelorMittal S.A., Essar Steel, Fives, NIPPON STEEL CORPORATION, Tata Steel Ltd., Ternium S.A., ThyssenKrupp AG, Voestalpine AG, NLMK, PJSC Magnitogorsk Iron and Steel Works, POSCO, Shandong Kerui Steel, and SSAB AB. The manufacturers are involved in mergers and acquisition which has a positive impact on the growth of the market. For instance, in November 2018, Arcelor Mittal S.A. acquired ILVA S.p.A., a distributor of iron and steel products in order to increase the company’s product portfolio in Europe. Additionally, in January 2018, Fives acquired Konecranes Machine Tool Service division in order to expand its product portfolio in machine tools service. The key companies are also increasing their investment activities in the European region to retain their stronghold in the market, For instance, in August 2019, ThyssenKrupp AG invested over 70 million euros in European sites. The aim of the company was to increase their business operation in the region. For each company, the report studies their presence, competitors, and product offerings, among others in Europe.

Europe Mg-Al-Zn Coated Steel Market:

- By Type

- Thin Carbon Steel

- Conventional Carbon Steel

- Thick Carbon Steel

- Special Made Carbon Steel

- By Application

- Automotive

- Construction

- Industrial Heating, Ventilation and Air Conditioning (HVAC)

- Electric Power Communication

- Specialized Greenhouse Structures

- Others

- By Country

- The UK

- Germany

- France

- Spain

- Italy

- Denmark

- Finland

- Iceland

- Sweden

- Norway

- Belgium

- The Netherlands

- Luxembourg

- Rest of Europe

Table of Contents

![]()

1. Market Scope

1.1. Market

Segmentation

1.2. Years

Considered

1.2.1. Historic

Years: 2013 - 2017

1.2.2. Base

Year: 2018

1.2.3. Forecast

Years: 2019 – 2027

2. Key Target Audiences

3. Research Methodology

3.1. Primary

Research

3.1.1. Research

Questionnaire

3.1.2. Europe

Percentage Breakdown

3.1.3. Primary

Interviews: Key Opinion Leaders (KOLs)

3.2. Secondary

Research

3.2.1. Paid

Databases

3.2.2. Secondary

Sources

3.3. Market

Size Estimates

3.3.1. Top-Down

Approach

3.3.2. Bottom-Up

Approach

3.4. Data

Triangulation Methodology

3.5. Research

Assumptions

4. Recommendations and Insights from AMI’s Perspective**

5. Holistic Overview of Mg-Al-Zn Coated Steel Market

6. Market Synopsis:

Mg-Al-Zn Coated Steel Market

7. Mg-Al-Zn Coated Steel Market Analysis: Qualitative

Perspective

7.1. Introduction

7.1.1. Product

Definition

7.1.2. Industry

Development

7.2. Market

Dynamics

7.2.1. Drivers

7.2.2. Restraints

7.2.3. Opportunities

7.3. Trends in

Mg-Al-Zn Coated Steel Market

7.4. Market

Determinants Radar Chart

7.5. Macro-Economic

and Micro-Economic Indicators: Mg-Al-Zn Coated Steel Market

7.6. Porter’s

Five Force Analysis

7.7. PESTEL

Analysis

7.8. Value

Chain Analysis

8. Europe Mg-Al-Zn Coated Steel Market Analysis and Forecasts,

2019 – 2027

8.1. Overview

8.1.1. Europe

Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

8.2. Europe

Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and Forecasts, By Type

8.2.1. Thin

Carbon Steel

8.2.1.1. Definition

8.2.1.2. Market Penetration, 2018

8.2.1.3. Market Estimation, 2013 – 2018

8.2.1.4. Market Forecast, 2019 – 2027

8.2.1.5. Compound Annual Growth Rate (CAGR)

8.2.1.6. Regional Bifurcation

8.2.1.6.1. France

8.2.1.6.1.1. Market Estimation, 2013 – 2018

8.2.1.6.1.2. Market Forecast, 2019 – 2027

8.2.1.6.2. The UK

8.2.1.6.2.1. Market Estimation, 2013 – 2018

8.2.1.6.2.2. Market Forecast, 2019 – 2027

8.2.1.6.3. Spain

8.2.1.6.3.1. Market Estimation, 2013 – 2018

8.2.1.6.3.2. Market Forecast, 2019 – 2027

8.2.1.6.4. Germany

8.2.1.6.4.1. Market Estimation, 2013 – 2018

8.2.1.6.4.2. Market Forecast, 2019 – 2027

8.2.1.6.5. Italy

8.2.1.6.5.1. Market Estimation, 2013 – 2018

8.2.1.6.5.2. Market Forecast, 2019 – 2027

8.2.1.6.6. Nordic Countries

8.2.1.6.6.1. Market Estimation, 2013 – 2018

8.2.1.6.6.2. Market Forecast, 2019 – 2027

8.2.1.6.7. Benelux Union

8.2.1.6.7.1. Market Estimation, 2013 – 2018

8.2.1.6.7.2. Market Forecast, 2019 – 2027

8.2.1.6.8. Rest of Europe

8.2.1.6.8.1. Market Estimation, 2013 – 2018

8.2.1.6.8.2. Market Forecast, 2019 – 2027

8.2.2. Conventional

Carbon Steel

8.2.2.1. Definition

8.2.2.2. Market Penetration, 2018

8.2.2.3. Market Estimation, 2013 – 2018

8.2.2.4. Market Forecast, 2019 – 2027

8.2.2.5. Compound Annual Growth Rate (CAGR)

8.2.2.6. Regional Bifurcation

8.2.2.6.1. France

8.2.2.6.1.1. Market Estimation, 2013 – 2018

8.2.2.6.1.2. Market Forecast, 2019 – 2027

8.2.2.6.2. The UK

8.2.2.6.2.1. Market Estimation, 2013 – 2018

8.2.2.6.2.2. Market Forecast, 2019 – 2027

8.2.2.6.3. Spain

8.2.2.6.3.1. Market Estimation, 2013 – 2018

8.2.2.6.3.2. Market Forecast, 2019 – 2027

8.2.2.6.4. Germany

8.2.2.6.4.1. Market Estimation, 2013 – 2018

8.2.2.6.4.2. Market Forecast, 2019 – 2027

8.2.2.6.5. Italy

8.2.2.6.5.1. Market Estimation, 2013 – 2018

8.2.2.6.5.2. Market Forecast, 2019 – 2027

8.2.2.6.6. Nordic Countries

8.2.2.6.6.1. Market Estimation, 2013 – 2018

8.2.2.6.6.2. Market Forecast, 2019 – 2027

8.2.2.6.7. Benelux Union

8.2.2.6.7.1. Market Estimation, 2013 – 2018

8.2.2.6.7.2. Market Forecast, 2019 – 2027

8.2.2.6.8. Rest of Europe

8.2.2.6.8.1. Market Estimation, 2013 – 2018

8.2.2.6.8.2. Market Forecast, 2019 – 2027

8.2.3. Thick

Carbon Steel

8.2.3.1. Definition

8.2.3.2. Market Penetration, 2018

8.2.3.3. Market Estimation, 2013 – 2018

8.2.3.4. Market Forecast, 2019 – 2027

8.2.3.5. Compound Annual Growth Rate (CAGR)

8.2.3.6. Regional Bifurcation

8.2.3.6.1. France

8.2.3.6.1.1. Market Estimation, 2013 – 2018

8.2.3.6.1.2. Market Forecast, 2019 – 2027

8.2.3.6.2. The UK

8.2.3.6.2.1. Market Estimation, 2013 – 2018

8.2.3.6.2.2. Market Forecast, 2019 – 2027

8.2.3.6.3. Spain

8.2.3.6.3.1. Market Estimation, 2013 – 2018

8.2.3.6.3.2. Market Forecast, 2019 – 2027

8.2.3.6.4. Germany

8.2.3.6.4.1. Market Estimation, 2013 – 2018

8.2.3.6.4.2. Market Forecast, 2019 – 2027

8.2.3.6.5. Italy

8.2.3.6.5.1. Market Estimation, 2013 – 2018

8.2.3.6.5.2. Market Forecast, 2019 – 2027

8.2.3.6.6. Nordic Countries

8.2.3.6.6.1. Market Estimation, 2013 – 2018

8.2.3.6.6.2. Market Forecast, 2019 – 2027

8.2.3.6.7. Benelux Union

8.2.3.6.7.1. Market Estimation, 2013 – 2018

8.2.3.6.7.2. Market Forecast, 2019 – 2027

8.2.3.6.8. Rest of Europe

8.2.3.6.8.1. Market Estimation, 2013 – 2018

8.2.3.6.8.2. Market Forecast, 2019 – 2027

8.2.4. Special

Made Carbon Steel

8.2.4.1. Definition

8.2.4.2. Market Penetration, 2018

8.2.4.3. Market Estimation, 2013 – 2018

8.2.4.4. Market Forecast, 2019 – 2027

8.2.4.5. Compound Annual Growth Rate (CAGR)

8.2.4.6. Regional Bifurcation

8.2.4.6.1. France

8.2.4.6.1.1. Market Estimation, 2013 – 2018

8.2.4.6.1.2. Market Forecast, 2019 – 2027

8.2.4.6.2. The UK

8.2.4.6.2.1. Market Estimation, 2013 – 2018

8.2.4.6.2.2. Market Forecast, 2019 – 2027

8.2.4.6.3. Spain

8.2.4.6.3.1. Market Estimation, 2013 – 2018

8.2.4.6.3.2. Market Forecast, 2019 – 2027

8.2.4.6.4. Germany

8.2.4.6.4.1. Market Estimation, 2013 – 2018

8.2.4.6.4.2. Market Forecast, 2019 – 2027

8.2.4.6.5. Italy

8.2.4.6.5.1. Market Estimation, 2013 – 2018

8.2.4.6.5.2. Market Forecast, 2019 – 2027

8.2.4.6.6. Nordic Countries

8.2.4.6.6.1. Market Estimation, 2013 – 2018

8.2.4.6.6.2. Market Forecast, 2019 – 2027

8.2.4.6.7. Benelux Union

8.2.4.6.7.1. Market Estimation, 2013 – 2018

8.2.4.6.7.2. Market Forecast, 2019 – 2027

8.2.4.6.8. Rest of Europe

8.2.4.6.8.1. Market Estimation, 2013 – 2018

8.2.4.6.8.2. Market Forecast, 2019 – 2027

8.3. Key

Segment for Channeling Investments

8.3.1. By Type

9. Europe Mg-Al-Zn Coated Steel Market Analysis and Forecasts,

2019 – 2027

9.1. Overview

9.2. Europe

Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and Forecasts, By Application

9.2.1. Automotive

9.2.1.1. Definition

9.2.1.2. Market Penetration, 2018

9.2.1.3. Market Estimation, 2013 – 2018

9.2.1.4. Market Forecast, 2019 – 2027

9.2.1.5. Compound Annual Growth Rate (CAGR)

9.2.1.6. Regional Bifurcation

9.2.1.6.1. France

9.2.1.6.1.1. Market Estimation, 2013 – 2018

9.2.1.6.1.2. Market Forecast, 2019 – 2027

9.2.1.6.2. The UK

9.2.1.6.2.1. Market Estimation, 2013 – 2018

9.2.1.6.2.2. Market Forecast, 2019 – 2027

9.2.1.6.3. Spain

9.2.1.6.3.1. Market Estimation, 2013 – 2018

9.2.1.6.3.2. Market Forecast, 2019 – 2027

9.2.1.6.4. Germany

9.2.1.6.4.1. Market Estimation, 2013 – 2018

9.2.1.6.4.2. Market Forecast, 2019 – 2027

9.2.1.6.5. Italy

9.2.1.6.5.1. Market Estimation, 2013 – 2018

9.2.1.6.5.2. Market Forecast, 2019 – 2027

9.2.1.6.6. Nordic Countries

9.2.1.6.6.1. Market Estimation, 2013 – 2018

9.2.1.6.6.2. Market Forecast, 2019 – 2027

9.2.1.6.7. Benelux Union

9.2.1.6.7.1. Market Estimation, 2013 – 2018

9.2.1.6.7.2. Market Forecast, 2019 – 2027

9.2.1.6.8. Rest of Europe

9.2.1.6.8.1. Market Estimation, 2013 – 2018

9.2.1.6.8.2. Market Forecast, 2019 – 2027

9.2.2. Construction

9.2.2.1. Definition

9.2.2.2. Market Penetration, 2018

9.2.2.3. Market Estimation, 2013 – 2018

9.2.2.4. Market Forecast, 2019 – 2027

9.2.2.5. Compound Annual Growth Rate (CAGR)

9.2.2.6. Regional Bifurcation

9.2.2.6.1. France

9.2.2.6.1.1. Market Estimation, 2013 – 2018

9.2.2.6.1.2. Market Forecast, 2019 – 2027

9.2.2.6.2. The UK

9.2.2.6.2.1. Market Estimation, 2013 – 2018

9.2.2.6.2.2. Market Forecast, 2019 – 2027

9.2.2.6.3. Spain

9.2.2.6.3.1. Market Estimation, 2013 – 2018

9.2.2.6.3.2. Market Forecast, 2019 – 2027

9.2.2.6.4. Germany

9.2.2.6.4.1. Market Estimation, 2013 – 2018

9.2.2.6.4.2. Market Forecast, 2019 – 2027

9.2.2.6.5. Italy

9.2.2.6.5.1. Market Estimation, 2013 – 2018

9.2.2.6.5.2. Market Forecast, 2019 – 2027

9.2.2.6.6. Nordic Countries

9.2.2.6.6.1. Market Estimation, 2013 – 2018

9.2.2.6.6.2. Market Forecast, 2019 – 2027

9.2.2.6.7. Benelux Union

9.2.2.6.7.1. Market Estimation, 2013 – 2018

9.2.2.6.7.2. Market Forecast, 2019 – 2027

9.2.2.6.8. Rest of Europe

9.2.2.6.8.1. Market Estimation, 2013 – 2018

9.2.2.6.8.2. Market Forecast, 2019 – 2027

9.2.3. Industrial

Heating, Ventilation and Air Conditioning (HVAC)

9.2.3.1. Definition

9.2.3.2. Market Penetration, 2018

9.2.3.3. Market Estimation, 2013 – 2018

9.2.3.4. Market Forecast, 2019 – 2027

9.2.3.5. Compound Annual Growth Rate (CAGR)

9.2.3.6. Regional Bifurcation

9.2.3.6.1. France

9.2.3.6.1.1. Market Estimation, 2013 – 2018

9.2.3.6.1.2. Market Forecast, 2019 – 2027

9.2.3.6.2. The UK

9.2.3.6.2.1. Market Estimation, 2013 – 2018

9.2.3.6.2.2. Market Forecast, 2019 – 2027

9.2.3.6.3. Spain

9.2.3.6.3.1. Market Estimation, 2013 – 2018

9.2.3.6.3.2. Market Forecast, 2019 – 2027

9.2.3.6.4. Germany

9.2.3.6.4.1. Market Estimation, 2013 – 2018

9.2.3.6.4.2. Market Forecast, 2019 – 2027

9.2.3.6.5. Italy

9.2.3.6.5.1. Market Estimation, 2013 – 2018

9.2.3.6.5.2. Market Forecast, 2019 – 2027

9.2.3.6.6. Nordic Countries

9.2.3.6.6.1. Market Estimation, 2013 – 2018

9.2.3.6.6.2. Market Forecast, 2019 – 2027

9.2.3.6.7. Benelux Union

9.2.3.6.7.1. Market Estimation, 2013 – 2018

9.2.3.6.7.2. Market Forecast, 2019 – 2027

9.2.3.6.8. Rest of Europe

9.2.3.6.8.1. Market Estimation, 2013 – 2018

9.2.3.6.8.2. Market Forecast, 2019 – 2027

9.2.4. Electric

Power Communication

9.2.4.1. Definition

9.2.4.2. Market Penetration, 2018

9.2.4.3. Market Estimation, 2013 – 2018

9.2.4.4. Market Forecast, 2019 – 2027

9.2.4.5. Compound Annual Growth Rate (CAGR)

9.2.4.6. Regional Bifurcation

9.2.4.6.1. France

9.2.4.6.1.1. Market Estimation, 2013 – 2018

9.2.4.6.1.2. Market Forecast, 2019 – 2027

9.2.4.6.2. The UK

9.2.4.6.2.1. Market Estimation, 2013 – 2018

9.2.4.6.2.2. Market Forecast, 2019 – 2027

9.2.4.6.3. Spain

9.2.4.6.3.1. Market Estimation, 2013 – 2018

9.2.4.6.3.2. Market Forecast, 2019 – 2027

9.2.4.6.4. Germany

9.2.4.6.4.1. Market Estimation, 2013 – 2018

9.2.4.6.4.2. Market Forecast, 2019 – 2027

9.2.4.6.5. Italy

9.2.4.6.5.1. Market Estimation, 2013 – 2018

9.2.4.6.5.2. Market Forecast, 2019 – 2027

9.2.4.6.6. Nordic Countries

9.2.4.6.6.1. Market Estimation, 2013 – 2018

9.2.4.6.6.2. Market Forecast, 2019 – 2027

9.2.4.6.7. Benelux Union

9.2.4.6.7.1. Market Estimation, 2013 – 2018

9.2.4.6.7.2. Market Forecast, 2019 – 2027

9.2.4.6.8. Rest of Europe

9.2.4.6.8.1. Market Estimation, 2013 – 2018

9.2.4.6.8.2. Market Forecast, 2019 – 2027

9.2.5. Specialized

Greenhouse Structures

9.2.5.1. Definition

9.2.5.2. Market Penetration, 2018

9.2.5.3. Market Estimation, 2013 – 2018

9.2.5.4. Market Forecast, 2019 – 2027

9.2.5.5. Compound Annual Growth Rate (CAGR)

9.2.5.6. Regional Bifurcation

9.2.5.6.1. France

9.2.5.6.1.1. Market Estimation, 2013 – 2018

9.2.5.6.1.2. Market Forecast, 2019 – 2027

9.2.5.6.2. The UK

9.2.5.6.2.1. Market Estimation, 2013 – 2018

9.2.5.6.2.2. Market Forecast, 2019 – 2027

9.2.5.6.3. Spain

9.2.5.6.3.1. Market Estimation, 2013 – 2018

9.2.5.6.3.2. Market Forecast, 2019 – 2027

9.2.5.6.4. Germany

9.2.5.6.4.1. Market Estimation, 2013 – 2018

9.2.5.6.4.2. Market Forecast, 2019 – 2027

9.2.5.6.5. Italy

9.2.5.6.5.1. Market Estimation, 2013 – 2018

9.2.5.6.5.2. Market Forecast, 2019 – 2027

9.2.5.6.6. Nordic Countries

9.2.5.6.6.1. Market Estimation, 2013 – 2018

9.2.5.6.6.2. Market Forecast, 2019 – 2027

9.2.5.6.7. Benelux Union

9.2.5.6.7.1. Market Estimation, 2013 – 2018

9.2.5.6.7.2. Market Forecast, 2019 – 2027

9.2.5.6.8. Rest of Europe

9.2.5.6.8.1. Market Estimation, 2013 – 2018

9.2.5.6.8.2. Market Forecast, 2019 – 2027

9.2.6. Others

9.2.6.1. Definition

9.2.6.2. Market Penetration, 2018

9.2.6.3. Market Estimation, 2013 – 2018

9.2.6.4. Market Forecast, 2019 – 2027

9.2.6.5. Compound Annual Growth Rate (CAGR)

9.2.6.6. Regional Bifurcation

9.2.6.6.1. France

9.2.6.6.1.1. Market Estimation, 2013 – 2018

9.2.6.6.1.2. Market Forecast, 2019 – 2027

9.2.6.6.2. The UK

9.2.6.6.2.1. Market Estimation, 2013 – 2018

9.2.6.6.2.2. Market Forecast, 2019 – 2027

9.2.6.6.3. Spain

9.2.6.6.3.1. Market Estimation, 2013 – 2018

9.2.6.6.3.2. Market Forecast, 2019 – 2027

9.2.6.6.4. Germany

9.2.6.6.4.1. Market Estimation, 2013 – 2018

9.2.6.6.4.2. Market Forecast, 2019 – 2027

9.2.6.6.5. Italy

9.2.6.6.5.1. Market Estimation, 2013 – 2018

9.2.6.6.5.2. Market Forecast, 2019 – 2027

9.2.6.6.6. Nordic Countries

9.2.6.6.6.1. Market Estimation, 2013 – 2018

9.2.6.6.6.2. Market Forecast, 2019 – 2027

9.2.6.6.7. Benelux Union

9.2.6.6.7.1. Market Estimation, 2013 – 2018

9.2.6.6.7.2. Market Forecast, 2019 – 2027

9.2.6.6.8. Rest of Europe

9.2.6.6.8.1. Market Estimation, 2013 – 2018

9.2.6.6.8.2. Market Forecast, 2019 – 2027

9.3. Key

Segment for Channeling Investments

9.3.1. By

Application

10. Europe Mg-Al-Zn Coated Steel Market Analysis and Forecasts,

2019 - 2027

10.1. Overview

10.1.1. Europe Mg-Al-Zn

Coated Steel Market Revenue (US$ Mn)

10.2. Europe

Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and Forecasts, By Type

10.2.1. Thin

Carbon Steel

10.2.2. Conventional

Carbon Steel

10.2.3. Thick

Carbon Steel

10.2.4. Special

Made Carbon Steel

10.3. Europe

Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and Forecasts, By Application

10.3.1. Automotive

10.3.2. Construction

10.3.3. Industrial

Heating, Ventilation and Air Conditioning (HVAC)

10.3.4. Electric

Power Communication

10.3.5. Specialized

Greenhouse Structures

10.3.6. Others

10.4. Europe

Mg-Al-Zn Coated Steel Market Revenue (US$ Mn), By Country

10.4.1. France

10.4.1.1. France Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Type

10.4.1.1.1. Thin Carbon Steel

10.4.1.1.2. Conventional Carbon Steel

10.4.1.1.3. Thick Carbon Steel

10.4.1.1.4. Special Made Carbon Steel

10.4.1.2. France Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Application

10.4.1.2.1. Automotive

10.4.1.2.2. Construction

10.4.1.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.1.2.4. Electric Power Communication

10.4.1.2.5. Specialized Greenhouse Structures

10.4.1.2.6. Others

10.4.2. The UK

10.4.2.1. The UK Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Type

10.4.2.1.1. Thin Carbon Steel

10.4.2.1.2. Conventional Carbon Steel

10.4.2.1.3. Thick Carbon Steel

10.4.2.1.4. Special Made Carbon Steel

10.4.2.2. The UK Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Application

10.4.2.2.1. Automotive

10.4.2.2.2. Construction

10.4.2.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.2.2.4. Electric Power Communication

10.4.2.2.5. Specialized Greenhouse Structures

10.4.2.2.6. Others

10.4.3. Spain

10.4.3.1. Spain Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Type

10.4.3.1.1. Thin Carbon Steel

10.4.3.1.2. Conventional Carbon Steel

10.4.3.1.3. Thick Carbon Steel

10.4.3.1.4. Special Made Carbon Steel

10.4.3.2. Spain Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Application

10.4.3.2.1. Automotive

10.4.3.2.2. Construction

10.4.3.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.3.2.4. Electric Power Communication

10.4.3.2.5. Specialized Greenhouse Structures

10.4.3.2.6. Others

10.4.4. Germany

10.4.4.1. Germany Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Type

10.4.4.1.1. Thin Carbon Steel

10.4.4.1.2. Conventional Carbon Steel

10.4.4.1.3. Thick Carbon Steel

10.4.4.1.4. Special Made Carbon Steel

10.4.4.2. Germany Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Application

10.4.4.2.1. Automotive

10.4.4.2.2. Construction

10.4.4.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.4.2.4. Electric Power Communication

10.4.4.2.5. Specialized Greenhouse Structures

10.4.4.2.6. Others

10.4.5. Italy

10.4.5.1. Italy Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Type

10.4.5.1.1. Thin Carbon Steel

10.4.5.1.2. Conventional Carbon Steel

10.4.5.1.3. Thick Carbon Steel

10.4.5.1.4. Special Made Carbon Steel

10.4.5.2. Italy Mg-Al-Zn Coated Steel Market Revenue (US$ Mn) and

Forecasts, By Application

10.4.5.2.1. Automotive

10.4.5.2.2. Construction

10.4.5.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.5.2.4. Electric Power Communication

10.4.5.2.5. Specialized Greenhouse Structures

10.4.5.2.6. Others

10.4.6. Nordic

Countries

10.4.6.1. Nordic Countries Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Type

10.4.6.1.1. Thin Carbon Steel

10.4.6.1.2. Conventional Carbon Steel

10.4.6.1.3. Thick Carbon Steel

10.4.6.1.4. Special Made Carbon Steel

10.4.6.2. Nordic Countries Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Application

10.4.6.2.1. Automotive

10.4.6.2.2. Construction

10.4.6.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.6.2.4. Electric Power Communication

10.4.6.2.5. Specialized Greenhouse Structures

10.4.6.2.6. Others

10.4.6.3. Nordic Countries Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Country

10.4.6.3.1. Denmark

10.4.6.3.2. Finland

10.4.6.3.3. Iceland

10.4.6.3.4. Sweden

10.4.6.3.5. Norway

10.4.7. Benelux

Union

10.4.7.1. Benelux Union Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Type

10.4.7.1.1. Thin Carbon Steel

10.4.7.1.2. Conventional Carbon Steel

10.4.7.1.3. Thick Carbon Steel

10.4.7.1.4. Special Made Carbon Steel

10.4.7.2. Benelux Union Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Application

10.4.7.2.1. Automotive

10.4.7.2.2. Construction

10.4.7.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.7.2.4. Electric Power Communication

10.4.7.2.5. Specialized Greenhouse Structures

10.4.7.2.6. Others

10.4.7.3. Benelux Union Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Country

10.4.7.3.1. Belgium

10.4.7.3.2. The Netherlands

10.4.7.3.3. Luxembourg

10.4.8. Rest of

Europe

10.4.8.1. Rest of Europe Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Type

10.4.8.1.1. Thin Carbon Steel

10.4.8.1.2. Conventional Carbon Steel

10.4.8.1.3. Thick Carbon Steel

10.4.8.1.4. Special Made Carbon Steel

10.4.8.2. Rest of Europe Mg-Al-Zn Coated Steel Market Revenue (US$ Mn)

and Forecasts, By Application

10.4.8.2.1. Automotive

10.4.8.2.2. Construction

10.4.8.2.3. Industrial Heating, Ventilation and Air Conditioning (HVAC)

10.4.8.2.4. Electric Power Communication

10.4.8.2.5. Specialized Greenhouse Structures

10.4.8.2.6. Others

10.5. Key

Segment for Channeling Investments

10.5.1. By

Country

10.5.2. By Type

10.5.3. By

Application

11. Competitive Benchmarking

11.1. Market

Share Analysis, 2018

11.2. Europe

Presence and Growth Strategies

11.2.1. Mergers

and Acquisitions

11.2.2. Product

Launches

11.2.3. Investments

Trends

11.2.4. R&D

Initiatives

12. Player Profiles

12.1. ArcelorMittal

S.A.

12.1.1. Company

Details

12.1.2. Company

Overview

12.1.3. Product

Offerings

12.1.4. Key

Developments

12.1.5. Financial

Analysis

12.1.6. SWOT

Analysis

12.1.7. Business

Strategies

12.2. Essar

Steel

12.2.1. Company

Details

12.2.2. Company

Overview

12.2.3. Product

Offerings

12.2.4. Key

Developments

12.2.5. Financial

Analysis

12.2.6. SWOT

Analysis

12.2.7. Business

Strategies

12.3. Fives

12.3.1. Company

Details

12.3.2. Company

Overview

12.3.3. Product

Offerings

12.3.4. Key

Developments

12.3.5. Financial

Analysis

12.3.6. SWOT

Analysis

12.3.7. Business

Strategies

12.4. Nippon

Steel Corporation

12.4.1. Company

Details

12.4.2. Company

Overview

12.4.3. Product

Offerings

12.4.4. Key

Developments

12.4.5. Financial

Analysis

12.4.6. SWOT

Analysis

12.4.7. Business

Strategies

12.5. NLMK

12.5.1. Company

Details

12.5.2. Company

Overview

12.5.3. Product

Offerings

12.5.4. Key

Developments

12.5.5. Financial

Analysis

12.5.6. SWOT

Analysis

12.5.7. Business

Strategies

12.6. PJSC

Magnitogorsk Iron and Steel Works

12.6.1. Company

Details

12.6.2. Company

Overview

12.6.3. Product

Offerings

12.6.4. Key

Developments

12.6.5. Financial

Analysis

12.6.6. SWOT

Analysis

12.6.7. Business

Strategies

12.7. POSCO

12.7.1. Company

Details

12.7.2. Company

Overview

12.7.3. Product

Offerings

12.7.4. Key

Developments

12.7.5. Financial

Analysis

12.7.6. SWOT

Analysis

12.7.7. Business

Strategies

12.8. Shandong

Kerui Steel

12.8.1. Company

Details

12.8.2. Company

Overview

12.8.3. Product

Offerings

12.8.4. Key

Developments

12.8.5. Financial

Analysis

12.8.6. SWOT

Analysis

12.8.7. Business

Strategies

12.9. SSAB AB

12.9.1. Company

Details

12.9.2. Company

Overview

12.9.3. Product

Offerings

12.9.4. Key

Developments

12.9.5. Financial

Analysis

12.9.6. SWOT

Analysis

12.9.7. Business

Strategies

12.10. Tata

Steel Ltd.

12.10.1. Company

Details

12.10.2. Company

Overview

12.10.3. Product

Offerings

12.10.4. Key

Developments

12.10.5. Financial

Analysis

12.10.6. SWOT

Analysis

12.10.7. Business

Strategies

12.11. Ternium

S.A.

12.11.1. Company

Details

12.11.2. Company

Overview

12.11.3. Product

Offerings

12.11.4. Key

Developments

12.11.5. Financial

Analysis

12.11.6. SWOT

Analysis

12.11.7. Business

Strategies

12.12. ThyssenKrupp

AG

12.12.1. Company

Details

12.12.2. Company

Overview

12.12.3. Product

Offerings

12.12.4. Key

Developments

12.12.5. Financial

Analysis

12.12.6. SWOT

Analysis

12.12.7. Business

Strategies

12.13. Voestalpine

AG

12.13.1. Company

Details

12.13.2. Company

Overview

12.13.3. Product

Offerings

12.13.4. Key

Developments

12.13.5. Financial

Analysis

12.13.6. SWOT

Analysis

12.13.7. Business

Strategies

12.14. Other

Market Participants

13. Key Findings

Note: This ToC is tentative and

can be changed according to the research study conducted during the course of

report completion.

**Exclusive for Multi-User and

Enterprise User.

At Absolute Markets Insights, we are engaged in building both global as well as country specific reports. As a result, the approach taken for deriving the estimation and forecast for a specific country is a bit unique and different in comparison to the global research studies. In this case, we not only study the concerned market factors & trends prevailing in a particular country (from secondary research) but we also tend to calculate the actual market size & forecast from the revenue generated from the market participants involved in manufacturing or distributing the any concerned product. These companies can also be service providers. For analyzing any country specifically, we do consider the growth factors prevailing under the states/cities/county for the same. For instance, if we are analyzing an industry specific to United States, we primarily need to study about the states present under the same(where the product/service has the highest growth). Similar analysis will be followed by other countries. Our scope of the report changes with different markets.

Our research study is mainly implement through a mix of both secondary and primary research. Various sources such as industry magazines, trade journals, and government websites and trade associations are reviewed for gathering precise data. Primary interviews are conducted to validate the market size derived from secondary research. Industry experts, major manufacturers and distributors are contacted for further validation purpose on the current market penetration and growth trends.

Prominent participants in our primary research process include:

- Key Opinion Leaders namely the CEOs, CSOs, VPs, purchasing managers, amongst others

- Research and development participants, distributors/suppliers and subject matter experts

Secondary Research includes data extracted from paid data sources:

- Reuters

- Factiva

- Bloomberg

- One Source

- Hoovers

Research Methodology

Key Inclusions